How to Write a Cheque in Canada

By Maude Gauthier | Published on 11 Jul 2023

Cheques are still a widely used method of payment. To write a cheque, simply order a cheque book and fill in all the necessary fields: date, amount, name of recipient, your signature and the memo.

Of course, many people have turned to more modern, digital payment methods. They’ve moved to Interac e-transfers or Canadian alternatives to Venmo. They’ve also compared credit cards to find the best one, sometimes resorting to prepaid cards. However, some people are not comfortable with digital technology. Not everyone can get a credit card, and the main drawback of prepaid cards is their low limits. Moreover, if you are new to Canada and you’ve just opened your bank account, are writing your first cheque or haven’t needed to write one before now, you need to learn how to fill out a cheque.

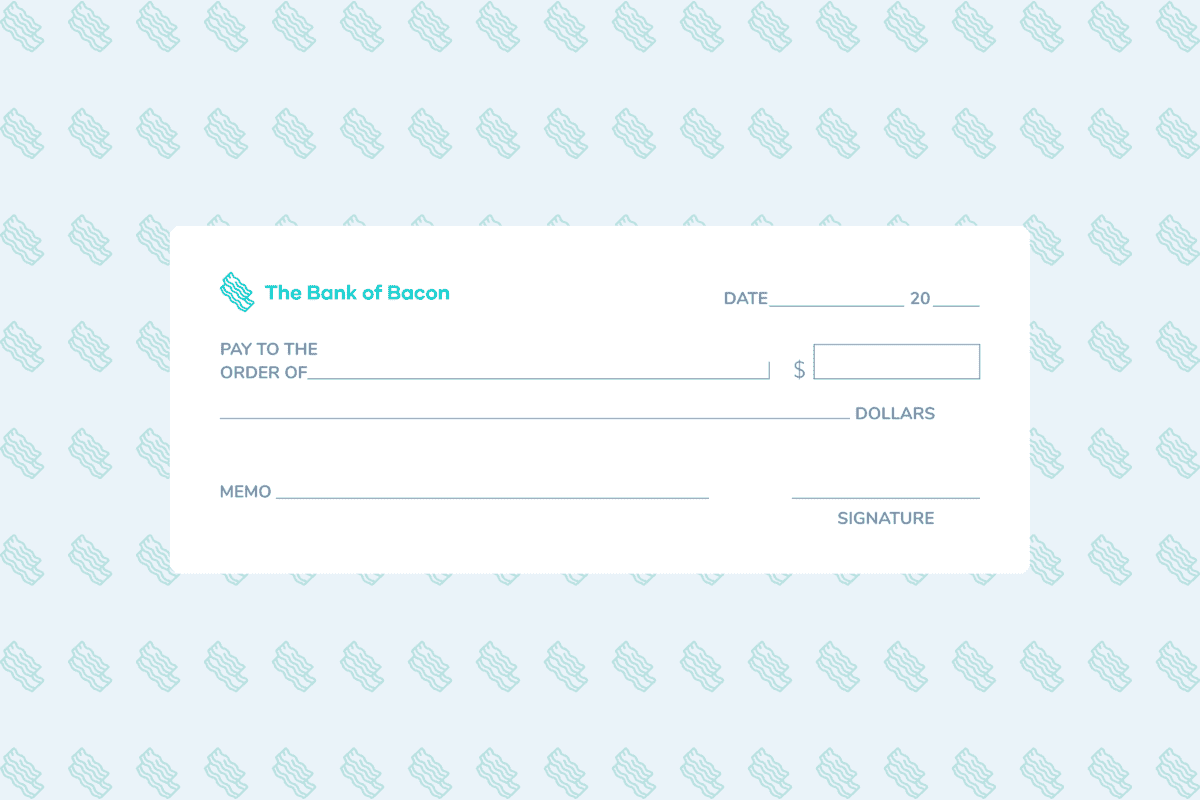

Cheque date

The date should be inscribed in the top right corner of the cheque. It represents the day it can be redeemed. Cheques can also be used after the due date has passed for up to six months. If you don’t have the necessary cash in your account but need to write a cheque to someone, you can post-date the cheque.

Recipient

On the “Pay to the order of” line, write the recipient’s name. This is one of the most crucial field, and you must ensure that the correct name with the proper spelling is written. The name could be that of a person, business, college, charitable organization, or any other institution with a bank account.

Amount

Simply begin writing your balance amount in the monetary amount box using numbers. It is best to start writing the numbers right after the printed $ symbol. This way, it leaves no room for anyone else to add more numbers. When writing the cents figure, make sure to use two decimals. You should write the number as “$125.50” and never as “$125.5.”

The next step is to type the same amount underneath the recipient’s name in the appropriate field. Although this is not required by law, it is strongly advised that you put your cheque amount in words as well. If the amount written in words does not match the amount entered in numerical format, the teller will accept the cheque for the amount written in words. You will write $654.32 as “six hundred fifty-four dollars and thirty-two cents” or “six hundred and fifty-four and 32/100.”

Signature

The bottom right corner of the cheque contains a signature line. Only use a readable signature that has been recorded with your bank. This signature validates the cheque and informs the bank that you have agreed to pay the specified amount to the recipient. Always sign the cheque after completing out all of the information and double-checking it. Your cheque will be invalidated if it does not contain a signature. Make sure to sign only in the appropriate places, as signatures are also used to rectify errors and substitute names and sums on cheques.

Memo

The memo area allows you to write a brief description or a note explaining why this cheque was made. An example of a memo could be a “Payment of fees for July” or “Rent payment for February.” It serves as a reminder of why you wrote the cheque. Furthermore, knowing the rationale for each payment makes it easier for you or for your accountant to treat the transaction appropriately. The memo line allows both parties to preserve a record of their payment and receipt details, which helps to minimize conflicts and uncertainty.

Understanding your cheque

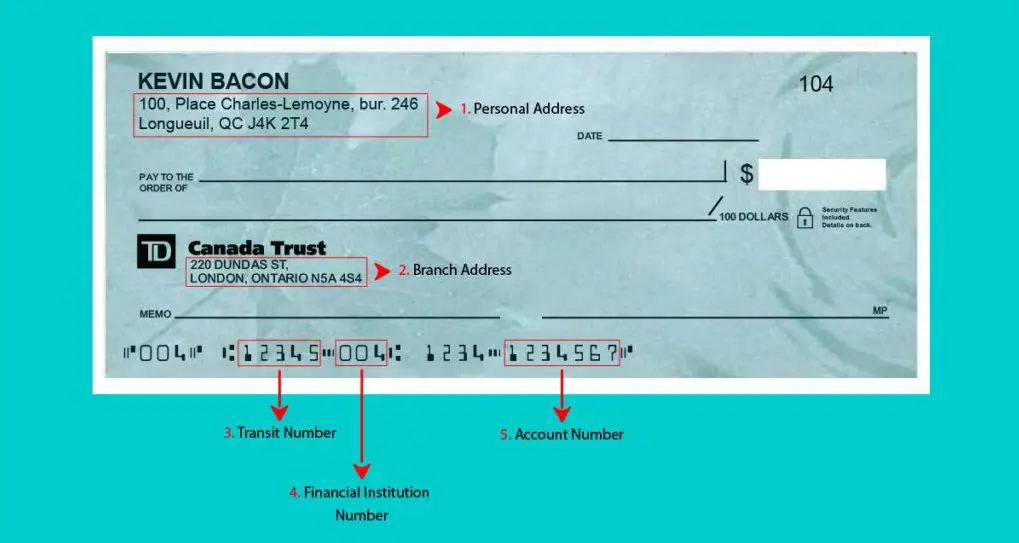

The numbers on a cheque serve as a guide. The person you pay by cheque does nothing more than deposit the cheque at their bank. Everything is processed electronically by the banks’ processing and payment systems.

Main aspects of a cheque include the names and addresses of the cheque writer and the bank, which are already pre-printed on every cheque. You can also include your phone number and address on the cheque by contacting your bank. The cheque number (top right) corresponds to the order of the cheque in the checkbook. The first cheque will be numbered 001, the second 002, and so on.

The transit number is used to locate your local bank, which is most likely where you opened the account. To avoid any misunderstanding, online banks with no physical branches may assign the same transit number to all their customers. Next, your banking institution is identified by the institution number. At the end of the series of digits is your account number.

The essential information you need to add is the date, the amount and your signature. Use a ballpoint pen or pencil with black or blue ink. We recommend that you indicate the payment amount in words, even if the law does not require it, as this is a protective measure if the amount in figures is disputed. To be on the safe side, you should also keep your checkbook in a safe place, and avoid pre-filling or signing cheques in advance.

Proper cheque etiquette

Accepting a cheque

When accepting a cheque, make sure that all essential fields are filled and that the cheque is signed. If the cheque is written out to more than one person, check if the reverse of the cheque has the needed signatures, also known as endorsements. For instance, if a cheque is made out to you and Andrew Jones, you must obtain Andrew Jones’ signature on the back of the cheque before your deposit if into the chequing account of your choice.

Cheque deposit

The old-fashioned way to cash a cheque is to take it to any bank branch where you have an account. The teller will ask for your debit card, and you will have to enter your PIN to validate your identity. You can also place the cheque in an envelope and use the ATM to cash it.

You can now cash your cheques by mobile deposit by photographing them with your phone. In this case, you should keep the original cheque between 5 and 15 days. A message usually appears at the same time as the deposit confirmation. It indicates the specific number of days as required by your financial institution. Once this period is over, destroy the cheque to avoid fraud.

The daily limit varies from bank to bank. For example, Desjardins allows you to deposit up to $10,000 in cheques per day, with a monthly limit of $100,000 whereas the National Bank limits your mobile cheque deposits to $50,000 per month.

Delays and holds

When you deposit a cheque, your bank adds the amount to your account balance. Depending on your bank’s rules, you may be able to use the funds immediately, or they may be held (frozen). Cheques take longer to clear when deposited on weekends, holidays and if they represent a large amount.

Government-regulated financial companies are required by law to limit the number of cheque holds. The Financial Consumer Agency of Canada (FCAC) website contains important information about your rights and obligations. If a person deposits a cheque in person at the bank, the first $100 is accessible immediately.

Stale-dated

Unless certified, cheques are deemed stale-dated after six months. A stale-dated cheque indicates that the item is beyond its expiration date but is not automatically invalid. These cheques may still be honored by banks, which are under no duty to do so. Cheques issued by the Government of Canada do not expire, and your bank may confirm that they are still valid.

Post-dated and NSF cheques

Cheques should not be cashed before their deposit date. However, some items may fall through the cracks due to the sheer volume of cheques and automated processing. If you find that a post-dated cheque has been cashed early, you can ask your financial institution to refund it up to the day before its deposit date. To pay the beneficiary, you’ll need to make other arrangements.

If you don’t have enough money in your account when someone tries to cash your cheque, it bounces. And when your cheque bounces, the bank charges you a NSF fee.

Alternatives to writing a cheque in Canada

If you’re still hesitant about using cheques, or don’t know how to write a cheque in Canada, there are several other payment methods available to you. Electronic payments are easy to use, as everything is automatically recorded and available at any time.

Interac e-Transfer

An Interac e-Transfer is a fast and secure way to transfer funds electronically to Canadian bank account holders. For international transfers, choose another platform, such as Wise.

To make an Interac e-Transfer, you must be able to access your banking services online or through an application. Simply click on this option. Transactions are usually instantaneous or take just a few minutes. The recipient receives an e-mail informing them that you’ve sent the money, and it’s easy for them to accept the transfer.

To cash the money, your recipient needs to know the answer to the security question you asked. This is one of the features that makes the system so secure. Electronic transfers have virtually replaced cheque writing. The process is faster, more convenient and safer.

Online money transfer with Wise

Wise was launched in 2011 as TransferWise. This fintech has its own payment network, offering cheaper and faster international money transfers than the payment system used by traditional banks to send money abroad (SWIFT). With wise, you have access to over 40 currencies and can send money to over 160 countries.

Wise started out as a money transfer solution for customers needing multi-currency international transfers but nowadays it includes payment with debit and credit cards, direct debit and bank transfer, as well as several features aimed at businesses. Each payment method has its own advantages and disadvantages in terms of costs and delivery times.

Paying with cryptocurrency

If you’re irritated by the archaic nature of paper cheques, you may want to try payment in cryptocurrency. If you and your recipient already own cryptocurrency assets, the transfer will be simple and easy. To do this, make sure you choose one of the best cryptocurrency platforms available, and you’re all set!

Writing a certified cheque

Writing a standard cheque isn’t always the best solution, even when the person you’re paying prefers paper! For large purchases, a certified cheque is recommended. It’s a lot like a personal cheque, only safer. The bank will add its seal to certify that the funds are available. This means that the recipient of your certified cheque will be sure that it won’t bounce and that they will be able to cash it without any problems.

Keeping track of the cheques you write

You need to make sure you have enough money in your account to pay for all the cheques you write. Keep a record of the cheques you sign, so you know which payments have been cashed and which are still outstanding. A cheque register is a booklet of your cheques, with a blank strip of paper on which you can write. Those who use their register fill in this strip of paper every time they write a cheque. The register lets you keep track of all the cheques you’ve written and write notes on each payment.

If you don’t have a cheque register, keep details of your cheques in an Excel or Google spreadsheet. In any case, it’s best to keep accurate information every time you write a cheque. Make a note of all the necessary information, such as the date, cheque number, cheque amount and name of the recipient.

Keeping track of the cheques you write will prevent you from getting into trouble and having to pay NSF charges if there are insufficient funds in your account. Always check that your cheque spending is consistent with your budget. Your register can also help protect you against identity theft and fraud by making it easier to detect suspicious transactions. Finally, proper tracking could help you avoid making duplicate payments! For example, you may have already paid your gardener or daycare provider with a cheque. But over time, you’ve forgotten about it. You then run the risk of making a double payment to the same person.

Security measures to write a cheque in Canada

Keep in mond some relatively simple but useful when writing a cheque. First, use clear, neat handwriting. Make sure that everything you’ve written is intelligible and leave no room for ambiguity. This is no time to get creative! Make sure that the signature you use is as natural as possible for you.

Then double-check all the information (date, amount, spelling). Don’t make any spelling mistakes that could make the recipient’s name appear to be someone else’s. Never give someone a blank cheque. Sign it only after you have entered all the information.

To increase the security of your cheque, never write the words “cash” or “bearer” on the “pay to” line. Cheques written in this way can be cashed by almost anyone. Giving or holding a blank cheque is tantamount to issuing a cheque payable to bearer.

After writing the recipient’s name and the amount in words, you need to draw additional horizontal lines. Without this precaution, fraudsters can place their name in front of the recipient’s and add the word “or”, implying that either person can cash the cheque.

If you’re mailing a cheque to someone, use an envelope with security features, or wrap it in a sheet of paper so that the cheque cannot be seen through the envelope. Keep your checkbook in a safe place at all times.

What to do if a mistake has been made while writing a cheque?

It is possible to write the incorrect name or amount by accident. To invalidate a cheque, you can write VOID in block letters, spanning all of the fields. Make sure to not write across the MICR line. To increase security, shred the cheque after it has been marked void. Voiding the cheque involves declaring a cheque invalid so that no one can use it. This step is critical in the process of limiting fraud or invalidating cheques.

Some errors can be crossed out with a simple strike and rewritten correctly. You must sign your name or initials next to these adjustments to convey to the bank that you accept them. If the errors are impossible to modify, you should destroy the cheque and use a new one.